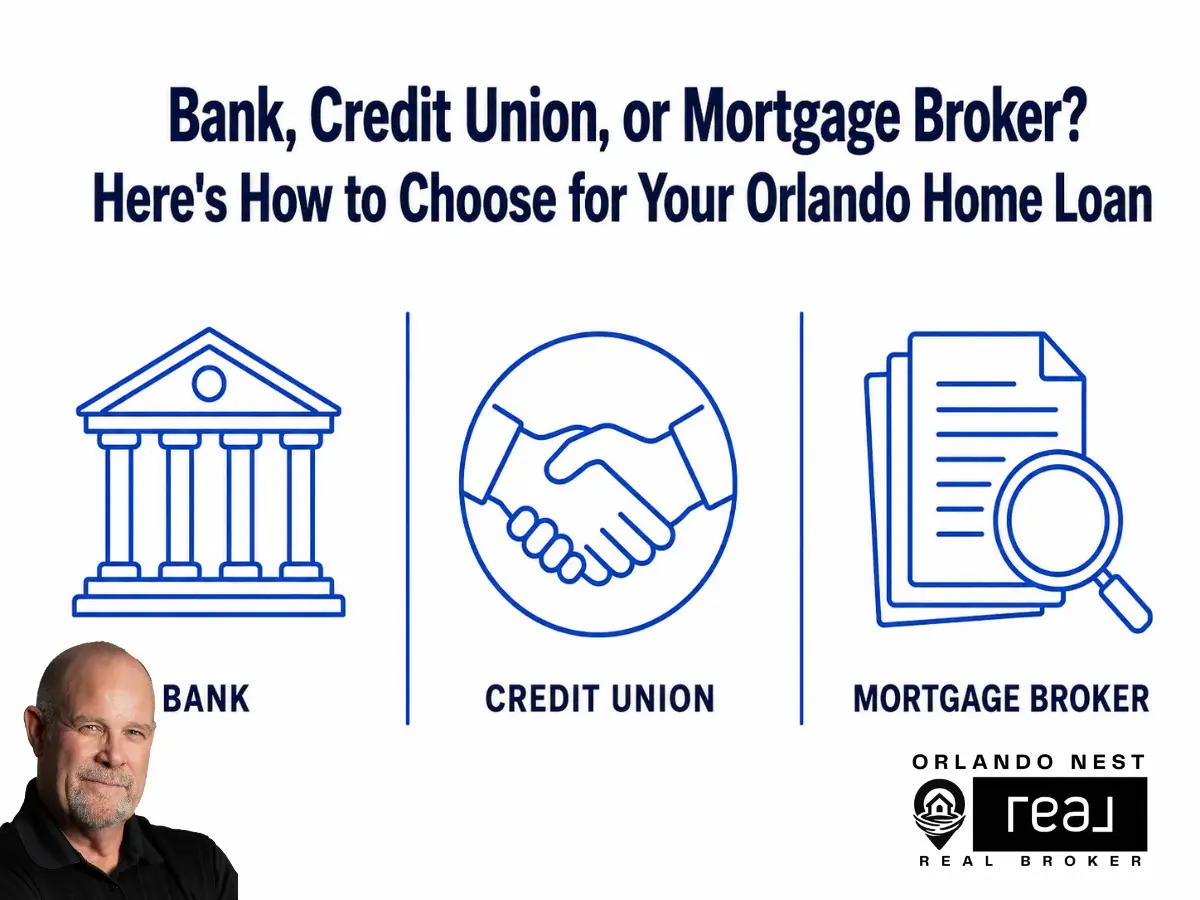

Most people spend more time picking out appliances than they do choosing a mortgage lender. That’s understandable — the lender conversation can feel intimidating, and most buyers just default to wherever they already bank. But the lender type you choose can affect your rate, your approval odds, and how smoothly your closing goes. In a market like Orlando, where buyers are often relocating from out of state and working against competitive timelines, it’s worth taking ten minutes to understand the difference.

Here’s a plain-English breakdown of the three main lender types, and who tends to be best served by each.

What Each Lender Type Actually Is

Banks

A traditional bank is a for-profit institution that lends its own money and earns revenue from the interest you pay. Loan officers at banks work for that institution — which means they can only offer products that bank carries. Big national banks have robust digital tools and the advantage of an existing relationship if you already bank there (some offer rate discounts or closing cost credits to current customers). The trade-off: banks carry higher overhead — branches, marketing, large executive teams — and that cost typically gets priced into your rate.

Credit Unions

A credit union looks a lot like a bank from the outside, but operates very differently under the hood. Credit unions are member-owned, not-for-profit cooperatives. Because they don’t answer to shareholders, they return profits to members in the form of lower rates and fees. According to data from the National Credit Union Administration, 30-year fixed mortgage rates at credit unions averaged roughly 0.13 percentage points lower than comparable bank rates in 2025 — a modest-sounding gap that translates to real savings over a 30-year loan. Credit unions also tend to have more flexible underwriting, which can make a meaningful difference for buyers who don’t fit the tightest conventional profile.

The catch: you have to qualify for membership. Requirements vary — some are tied to your employer or profession, others to where you live or worship. In Central Florida, several credit unions have relatively easy membership paths for local residents.

Mortgage Brokers

A mortgage broker doesn’t lend money directly. Instead, brokers act as intermediaries between you and a network of wholesale lenders — sometimes 20 to 50 or more. They take your application, shop it across multiple lenders, and bring you the best available terms. Because wholesale lenders don’t have retail overhead, the pricing they offer brokers is often lower than what that same lender would quote you walking in off the street.

Brokers typically disclose exactly what they earn on a transaction — this is required by federal law — and are paid either by the lender, by you, or a combination. For buyers with complex situations (non-traditional income, a credit score at the edge of qualifying, or a specialty loan like a VA purchase), a broker’s ability to shop across lenders can make a significant difference.

The Rate Reality

Rates vary by borrower, loan type, and timing — but in general, the pricing hierarchy runs roughly like this: large banks tend to be most expensive because of retail overhead; credit unions and smaller community lenders tend to be more competitive; and mortgage brokers operating at wholesale pricing can often come in below both, particularly for buyers who take the time to shop.

That said, rate alone doesn’t tell the whole story. Origination fees, points, closing costs, and how your loan is serviced after closing all affect the total picture. The CFPB’s mortgage comparison tool lets you evaluate lenders on an apples-to-apples basis using APR, which folds in most of those costs.

| Bank | Credit Union | Mortgage Broker | |

| Who can use it? | Anyone | Members only (joining usually easy) | Anyone |

| Who holds your money? | For-profit institution | Member-owned nonprofit | Doesn’t lend — shops lenders |

| Rate potential | Retail pricing; higher overhead | Often 0.1%–0.4% lower than banks | Wholesale pricing; potentially lowest |

| Loan product variety | Wide range | Moderate; varies by CU | Widest — access to many lenders |

| VA/FHA loan access | Varies by institution | Some; check before assuming | Broad access; VA-savvy brokers common |

| Personalized service | Varies | Typically high | Typically high |

| Technology / digital tools | Usually strong | Often limited | Varies by broker |

| Best for… | Existing customers; straightforward profiles | First-timers; flexible credit; lower fees | Complex situations; VA; rate shopping |

A Note for VA Loan Buyers

If you’re using a VA loan — which allows eligible veterans, active-duty service members, and qualifying surviving spouses to buy with no down payment and no private mortgage insurance — your lender choice matters in a specific way. Not every lender handles VA loans well. Some larger retail banks process them infrequently and may lack the internal expertise to navigate VA appraisal requirements or funding fee structures efficiently.

Specialty VA lenders and experienced mortgage brokers who work with VA-approved wholesale lenders tend to close VA loans faster and with fewer complications. According to the Department of Veterans Affairs, more than 58,000 VA-eligible buyers each year forgo their VA benefit and use conventional financing instead — often because of misconceptions about the process. If you qualify, it’s worth talking to a lender who has specific, current experience with VA loans in Florida.

For more on using your VA benefit in Orlando, see our VA resources at https://orlandonest.com/va-wealth-guide.

For Buyers Relocating to Orlando

If you’re moving here from another state, you’re likely dealing with a bank you’ve used for years in your old city. That institution may or may not be a strong lender in the Florida market. Florida has specific insurance and disclosure requirements that affect closing, and local lenders — whether credit unions or brokers with Florida-specific lender relationships — are often more familiar with those nuances.

It’s worth getting at least one competing quote from a Florida-based lender or broker before locking. You’re not obligated to switch, but the data comparison is almost always useful.

What is the main difference between a mortgage broker and a bank for a home loan in Florida?

A bank lends you its own money and can only offer its own loan products. A mortgage broker doesn’t lend money at all — they shop your application across a network of wholesale lenders to find the best available rate and terms. Banks price loans at retail; brokers typically access wholesale pricing, which can be lower. The right choice depends on your financial profile, loan type, and how much time you want to spend comparing options yourself.

Are credit union mortgage rates really lower than bank rates?

On average, yes. According to the National Credit Union Administration, 30-year fixed mortgage rates at credit unions ran approximately 0.13 percentage points below comparable bank rates in 2025. That gap may seem small, but it compounds meaningfully over a 30-year loan. Credit unions also typically charge lower origination fees and closing costs. The trade-off is that you must qualify for membership, and not every credit union offers the full range of loan products.

Should a VA loan buyer use a bank, credit union, or mortgage broker?

Any of the three can originate VA loans, but lender experience matters significantly with VA financing. Banks that process VA loans infrequently may be slower and less familiar with VA appraisal requirements or funding fee structures. Specialty VA lenders and experienced mortgage brokers who work regularly with VA-approved wholesale lenders tend to close VA loans more efficiently. If you’re using a VA benefit, prioritize working with a lender who can demonstrate current, hands-on experience with VA transactions in Florida.

Do I pay a mortgage broker directly, or does the lender pay them?

Federal law requires mortgage brokers to disclose their compensation upfront. Brokers are typically paid by the lender through a lender credit (called yield spread premium), by you directly through an origination fee, or sometimes a combination of both. Importantly, they cannot be compensated by both sides of the transaction on the same loan. Because brokers access wholesale pricing, even after their fee is factored in, the total cost is often competitive with or lower than going direct to a retail bank.

Can I use a mortgage broker if I’m relocating to Orlando from another state?

Yes, and it’s often a smart move. A mortgage broker who works regularly in the Florida market will have relationships with lenders familiar with Florida’s specific closing requirements, flood insurance obligations, and disclosure rules. If you’re relocating and already have a long-standing bank relationship, it’s worth getting a competing quote from a Florida-based broker before locking — even if you ultimately stick with your current bank. The comparison costs you nothing and often surfaces a better offer.

Does it matter which lender I choose if I’m a first-time buyer in Orlando?

Yes, especially around qualification flexibility and fees. First-time buyers are more likely to sit near the edge of credit or income thresholds, and different lender types underwrite differently. Credit unions tend to have more flexible guidelines and lower fees. Mortgage brokers can shop your application to find the lender most likely to approve your profile at the best rate. Some lenders also have specific first-time buyer programs — including connections to Florida Housing Finance Corporation programs that offer down payment assistance. Your lender choice can affect whether you qualify at all, not just what rate you get.

What does “preapproval” mean, and does it matter which lender type gives it to me?

Preapproval means a lender has reviewed your credit, income, and assets and issued a conditional commitment to lend up to a specified amount. It carries more weight than prequalification, which is based only on unverified self-reported information. In Orlando’s market, sellers and listing agents take preapproval seriously — it signals you’re a credible buyer. The lender type doesn’t change what preapproval means, but lender reputation can matter: a preapproval from a well-known lender or one the listing agent has worked with before can carry slightly more weight in a competitive offer situation.

Which One Is Right for You?

There’s no universal right answer, but there’s usually a best fit for your situation:

- You’re a first-time buyer with a solid but not exceptional credit profile and want lower fees: a credit union is worth exploring first.

- You have an existing relationship with a national bank and a straightforward financial picture: going direct may be convenient and competitive enough.

- You’re a VA loan buyer, self-employed, have non-traditional income, or want someone to actively shop your application across multiple lenders: a mortgage broker is likely your strongest move.

- You’re relocating from out of state and unfamiliar with Florida lenders: get at least one quote from a Florida-based broker or credit union alongside whatever your current bank offers.

Whichever direction you go, get preapproved before you start shopping seriously. In Orlando’s market, sellers take preapproved buyers significantly more seriously than pre-qualified ones — and knowing your actual number shapes every other decision you make.

Ted’s Take

The question I get most often from buyers is ‘should I just use my bank?’ And my honest answer is: maybe, but find out first. The buyers I’ve seen leave money on the table almost always skipped the comparison step — they called their bank, got a number, and figured that was the market. It often isn’t. The 15 minutes it takes to get a competing quote from a credit union or broker has saved buyers I work with thousands of dollars at the closing table. And for military buyers specifically: if you’re entitled to a VA loan and your lender isn’t talking about it enthusiastically, find one who is.

Ted Moseley is a Central Florida REALTOR® with Orlando Nest – Real Broker, LLC, helping buyers and sellers make clear, data-driven decisions across Orlando, Winter Park, Lake Nona, College Park, and surrounding neighborhoods.

Explore: Market Update · Home Value · Sell a Home · Reviews · More Articles

Have a question about timing, pricing, or next steps? Schedule a quick 30-minute call →

© Ted Moseley – Orlando Nest – Real Broker, LLC